Planning for retirement is a significant milestone in life, especially for those born in 1959. If you're in this group, understanding the concept of "full retirement age 1959" is crucial for making informed decisions about your financial future. Full retirement age (FRA) refers to the age at which you can receive your full Social Security retirement benefits without any reduction. For individuals born in 1959, this age is a pivotal factor that determines when you can access your benefits in their entirety. Knowing your FRA helps you plan better, ensuring you maximize your retirement income while avoiding unnecessary penalties.

Retirement planning can seem overwhelming, but breaking it down into manageable steps makes it easier to navigate. The Social Security Administration (SSA) has set specific guidelines to determine the full retirement age for different birth years. For those born in 1959, your FRA falls between 66 and 67 years, depending on the exact month of your birth. Understanding this timeline is essential, as it influences when you should start claiming your benefits. Delaying your claim beyond your FRA can even increase your monthly payments, providing a financial cushion in your later years.

With retirement on the horizon, it's important to explore all aspects of full retirement age 1959, from its definition to its implications. This guide will delve into the intricacies of Social Security benefits, strategies for optimizing your retirement income, and frequently asked questions about the topic. By the end of this article, you'll have a clearer understanding of how to make the most of your retirement years while ensuring financial stability. Let’s dive in and uncover everything you need to know about full retirement age 1959.

Read also:Exploring The Life And Career Of Stormy Daniels The Erotic Star Who Captivated A Nation

Table of Contents

- What Is Full Retirement Age 1959?

- Why Does Full Retirement Age Matter for Those Born in 1959?

- How to Calculate Your Full Retirement Age

- What Happens If You Retire Early?

- Benefits of Waiting Until Full Retirement Age

- Common Misconceptions About Full Retirement Age

- How to Plan for Retirement at Full Retirement Age 1959

- Frequently Asked Questions About Full Retirement Age 1959

What Is Full Retirement Age 1959?

Full retirement age (FRA) is the age at which individuals can claim their full Social Security retirement benefits without any reduction. For those born in 1959, the FRA is a critical milestone that determines when they can access their benefits in full. The Social Security Administration (SSA) has gradually increased the FRA for individuals born after 1937, and for those born in 1959, it falls between 66 and 67 years, depending on the month of birth.

The concept of full retirement age was introduced to ensure that Social Security benefits align with life expectancy and economic factors. For instance, individuals born in 1959 will reach their FRA at 66 years and 10 months. This means that if you were born in January 1959, your FRA would be October 2025, while those born in December 1959 will reach their FRA in August 2026. Understanding this timeline is essential for planning your retirement and ensuring you make the most of your benefits.

It's worth noting that full retirement age 1959 is not the same as the age of eligibility for Medicare or other retirement programs. While Medicare benefits typically begin at age 65, Social Security benefits depend on your FRA. Knowing the distinction between these programs can help you avoid confusion and ensure you’re prepared for all aspects of retirement. By understanding what full retirement age 1959 entails, you can make informed decisions about when to claim your benefits and how to optimize your retirement income.

Why Does Full Retirement Age Matter for Those Born in 1959?

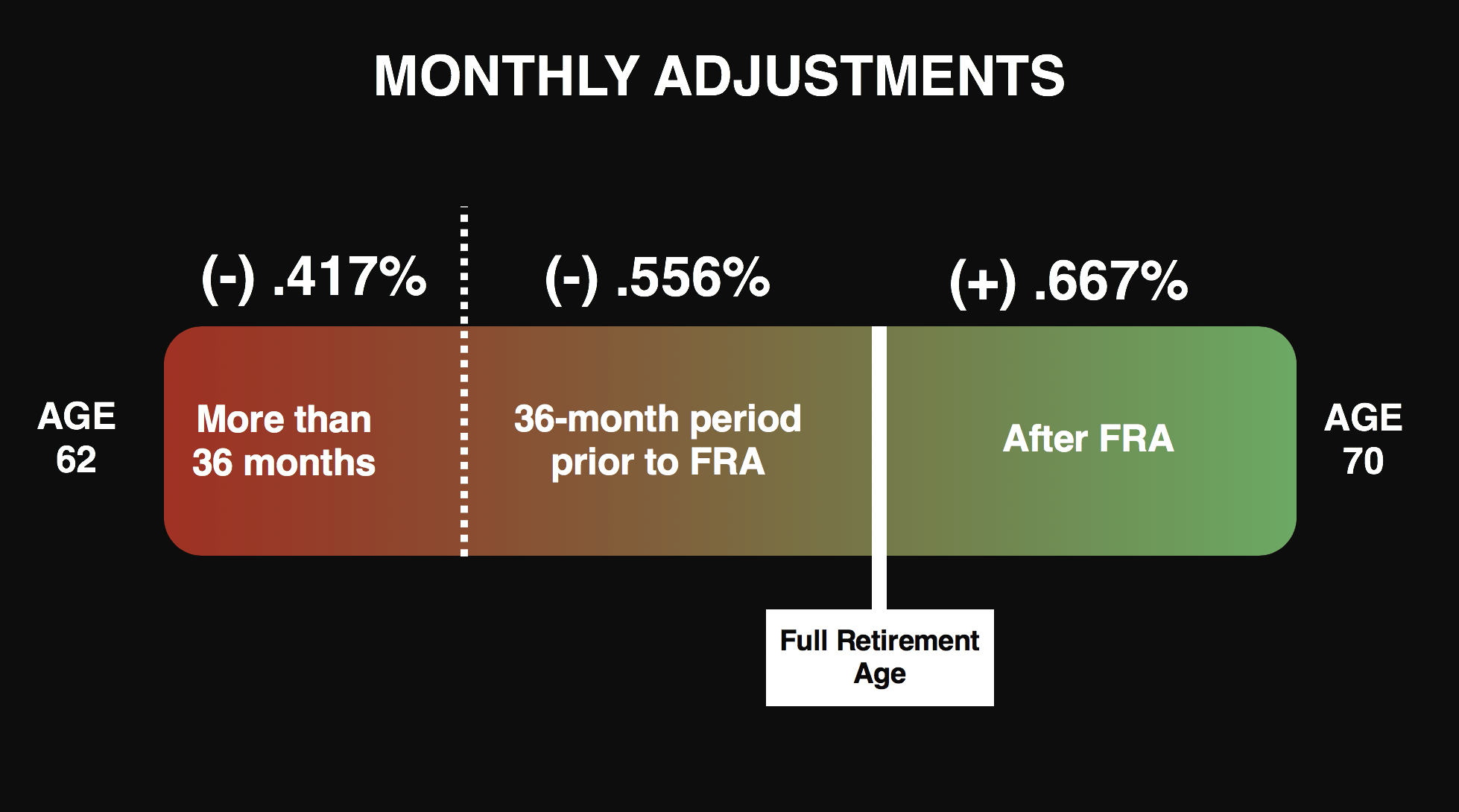

Understanding why full retirement age 1959 matters is crucial for anyone planning their retirement. The FRA is not just a number; it has significant implications for your financial well-being during your retirement years. One of the primary reasons it matters is that claiming benefits before your FRA results in a permanent reduction in your monthly payments. For individuals born in 1959, retiring at 62—the earliest age to claim benefits—means receiving only 70% of your full benefit amount.

On the other hand, waiting until your FRA ensures you receive 100% of your entitled benefits. This can make a substantial difference in your monthly income, especially if you plan to rely heavily on Social Security during retirement. Additionally, delaying your benefits beyond your FRA can increase your payments by up to 8% per year until age 70, providing an even greater financial cushion. For those born in 1959, this means you could potentially increase your benefits by waiting until 2029 to claim them.

What Are the Financial Implications of Full Retirement Age?

The financial implications of full retirement age 1959 are multifaceted. First, your FRA directly impacts the amount of money you’ll receive each month. If you claim benefits early, your payments will be reduced for the rest of your life. This reduction is calculated based on the number of months you claim before reaching your FRA. For example, if your FRA is 66 and 10 months, claiming at 62 reduces your benefits by approximately 30%.

Read also:Understanding Croup Cough Causes Symptoms And Treatments

Second, the timing of your benefits affects your long-term financial stability. If you retire early and claim reduced benefits, you may face challenges if you outlive your savings. Conversely, waiting until your FRA or later ensures you receive the maximum possible benefit, which can provide greater financial security. This is especially important for individuals born in 1959, as life expectancy continues to increase, and many retirees may need their benefits to last 20–30 years or more.

How to Calculate Your Full Retirement Age

Calculating your full retirement age 1959 is a straightforward process, but it requires attention to detail. The Social Security Administration provides a clear schedule that outlines the FRA for each birth year. For individuals born in 1959, the FRA is 66 years and 10 months. To determine your exact FRA, you’ll need to know your birth month, as this influences the specific month you’ll reach your FRA.

For example, if you were born in January 1959, your FRA would be October 2025. If you were born in December 1959, your FRA would fall in August 2026. Knowing this timeline is essential for planning your retirement and deciding when to claim your benefits. To simplify the process, you can use the SSA’s online retirement age calculator, which provides personalized information based on your birth date.

What Factors Influence Your Full Retirement Age?

Several factors influence your full retirement age 1959, including your birth year and month. However, other considerations, such as your financial situation and health, can also impact your decision to claim benefits early or delay them. For instance, if you have sufficient savings and are in good health, waiting until your FRA or later may be advantageous. On the other hand, if you face financial challenges or health issues, claiming benefits early might be a more practical choice.

What Happens If You Retire Early?

Retiring early can be tempting, especially if you’re ready to leave the workforce. However, claiming Social Security benefits before your full retirement age 1959 comes with significant drawbacks. The most notable consequence is a permanent reduction in your monthly payments. For those born in 1959, retiring at 62 results in a 30% reduction in benefits, which can have long-term financial implications.

Additionally, early retirees may face challenges if they outlive their savings. With life expectancy increasing, many retirees need their benefits to last 20–30 years or more. Claiming reduced benefits early can strain your finances, leaving you with less income during your later years. It’s essential to weigh the pros and cons of early retirement carefully and consider how it aligns with your overall financial goals.

Are There Benefits to Retiring Early?

While retiring early has its drawbacks, it’s not without its advantages. For some individuals, early retirement offers the opportunity to enjoy more time with family, pursue hobbies, or focus on personal interests. If you have other sources of income, such as a pension or savings, retiring early may be a viable option. However, it’s crucial to ensure that your financial foundation is solid before making this decision.

Benefits of Waiting Until Full Retirement Age

Waiting until your full retirement age 1959 offers several advantages, the most significant being the ability to claim your full Social Security benefits. For individuals born in 1959, this means receiving 100% of your entitled benefits, which can provide greater financial stability during retirement. Additionally, delaying your benefits beyond your FRA can increase your payments by up to 8% per year until age 70, offering an even greater financial cushion.

Another benefit of waiting is the potential to maximize your retirement income. By claiming benefits at your FRA or later, you ensure that your monthly payments are as high as possible. This can be especially beneficial if you plan to rely heavily on Social Security during retirement. For those born in 1959, waiting until 2029 to claim benefits could result in a significant increase in monthly payments, providing greater financial security.

Common Misconceptions About Full Retirement Age

There are several misconceptions about full retirement age 1959 that can lead to poor financial decisions. One common myth is that Social Security benefits are only available at age 65. While Medicare benefits begin at 65, Social Security benefits depend on your FRA, which is 66 and 10 months for those born in 1959. Another misconception is that claiming benefits early won’t significantly impact your income. In reality, early claims result in a permanent reduction in benefits.

How to Plan for Retirement at Full Retirement Age 1959

Planning for retirement at your full retirement age 1959 requires a strategic approach. Start by assessing your financial situation, including your savings, investments, and other sources of income. Next, consider how Social Security benefits fit into your overall retirement plan. If possible, delay claiming benefits until your FRA or later to maximize your monthly payments.

Frequently Asked Questions About Full Retirement Age 1959

What Is the Full Retirement Age for Someone Born in 1959?

The full retirement age for someone born in 1959 is 66 years and 10 months. This means individuals born in 1959 will reach their FRA between October 2025 and August 2026, depending on their birth month.

Can I Work While Receiving Social Security Benefits?

Yes, you can work while receiving Social Security benefits, but your earnings may affect your payments if you haven’t reached your full retirement age 1959. The SSA applies an earnings test to determine if your benefits should be reduced.

How Can I Maximize My Social Security Benefits?

To maximize your Social Security benefits, consider delaying your claim until your full retirement age or later. Additionally, ensure you have accurate earnings records, as your benefits are based on your highest 35 years of earnings.

In conclusion, understanding full retirement age 1959 is essential for making informed decisions about your retirement. By planning strategically and considering the implications of your choices, you can ensure a financially secure future. For more information, visit the Social Security Administration’s website.